Wildfire Preparedness and Insurance Are Now Closing Issues in Rim Country

By Dennis R. Riccio, President, Central Arizona Association of Realtors

The Rim Country real estate market did not slow down this spring. It matured.

Buyers remained active. Sellers brought more homes to market. And the difference between a successful listing and a stale listing increasingly came down to price, preparation, presentation, and local expertise.

Earlier this year, I wrote that the Mogollon Rim was not following the same script as many national housing headlines. That remains true. Our market continues to benefit from lifestyle demand, long-term ownership, limited land availability, and buyers who see Rim Country as more than a place to purchase property.

But spring added important context. Resilience does not mean every listing performs the same way.

Rim Country remains strong, but it is no longer simple. The market is active, but more selective. Inventory has improved. Buyers have more room to compare. Sellers face more competition. And success now depends less on momentum and more on discipline, preparation, pricing accuracy, and professional execution.

This is not a broad-based market decline. It is a more balanced, more selective, and more professional market.

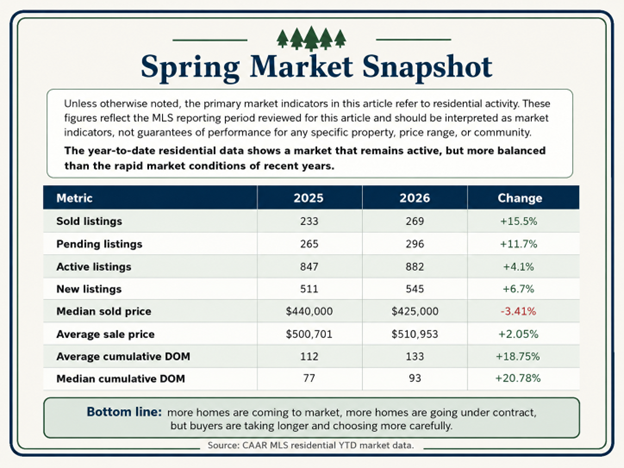

The Spring Market Snapshot below summarizes the primary year-to-date residential indicators reviewed for this article. These figures should be interpreted as market indicators, not guarantees of performance for any specific property, price range, or community.

For REALTORS® and brokers, that is the key interpretation. The market is not giving us a simple headline. It is giving us a professional market that requires explanation.

In March, the CAAR market was still showing signs of supply constraint. Active listings were slightly below the prior year, and the market continued to stand apart from many national housing headlines. In that earlier report, residential sales were up more than 27% year over year, active listings were down 3.7%, absorption was 5.33 months, new listings were up 12%, and pending listings were up 12.3%.

As spring progressed, more sellers entered the market. By April, active residential listings had moved modestly higher, and year-to-date new listings were also ahead of last year.

That shift does not contradict the earlier trend. It explains the spring market.

Rim Country moved from tighter inventory into a more balanced seasonal environment. Buyers gained more choices, but demand remained present, as shown by increases in both sold and pending activity.

In other words, the market did not reverse course. It broadened.

That distinction matters when we are talking with clients. Sellers may hear “more inventory” and assume the market has weakened. Buyers may hear “more sales” and assume they have missed their opportunity. Neither interpretation is complete. The correct message is more nuanced: activity remains healthy, but the market is more competitive and more selective.

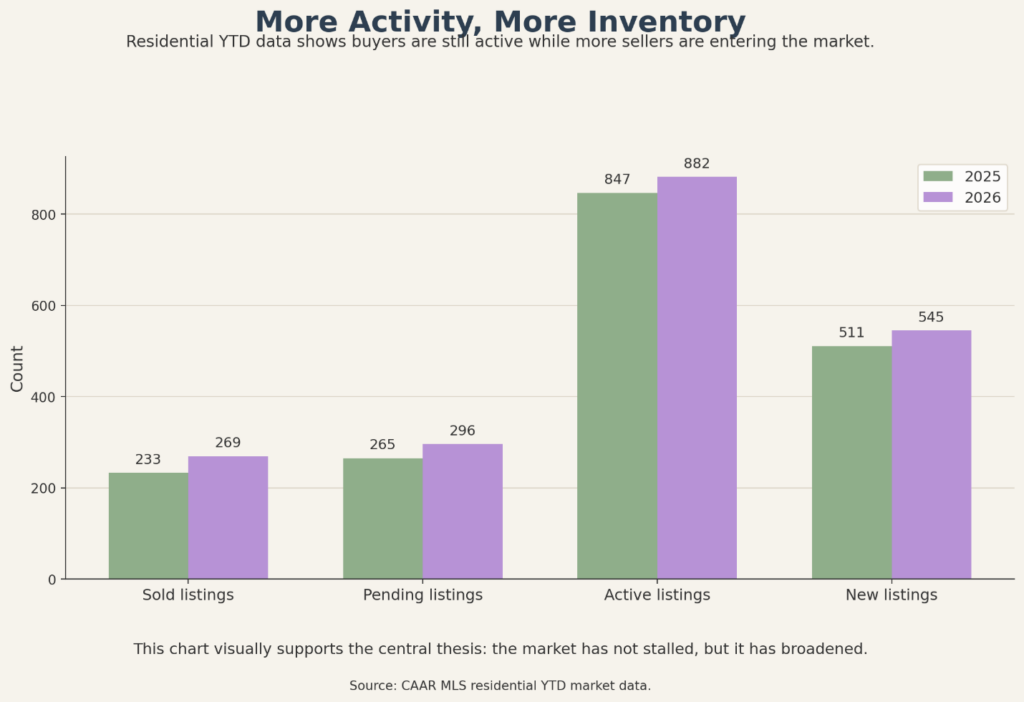

Residential YTD data shows buyers are still active while more sellers are entering the market.

The most important thing to understand is that buyers have not disappeared.

Year-to-date residential sold listings are up 15.5%, and pending listings are up 11.7%. Those are not signs of a stalled market. They show that buyers are still writing contracts, still closing transactions, and still responding to properties that meet their expectations.

But the nature of buyer activity has changed.

Buyers are not acting with the same urgency we saw during the most compressed inventory periods. They are comparing more options. They are paying closer attention to condition. They are looking carefully at price, insurance, financing, repairs, access, and long-term value.

Elevated borrowing costs and affordability concerns remain part of the buyer psychology, even in a lifestyle-driven market like ours. The difference is that Rim Country demand is often supported by lifestyle motivation, equity from other markets, second-home interest, retirement planning, and long-term relocation goals.

This is a market with demand, but not automatic demand.

That distinction matters.

For brokers and agents, this is where client counseling becomes critical. A seller who sees increased sales activity may assume the market will absorb any price. A buyer who sees longer days on market may assume every seller is negotiable. The data does not support either extreme. The real picture is disciplined demand: buyers are present, but they are more value-focused and less willing to overlook pricing or condition issues.

Inventory improved this spring, and that changed the tone of the market.

Active residential listings increased slightly in April, from 460 in April 2025 to 468 in April 2026. In the year-to-date reporting column, active listings increased from 847 to 882, while new listings increased from 511 to 545.

That gives buyers more choice than they had during tighter periods.

For sellers, this means the market is less forgiving. A property is no longer competing only against limited supply. It is competing against other homes in the same price range, condition category, and location.

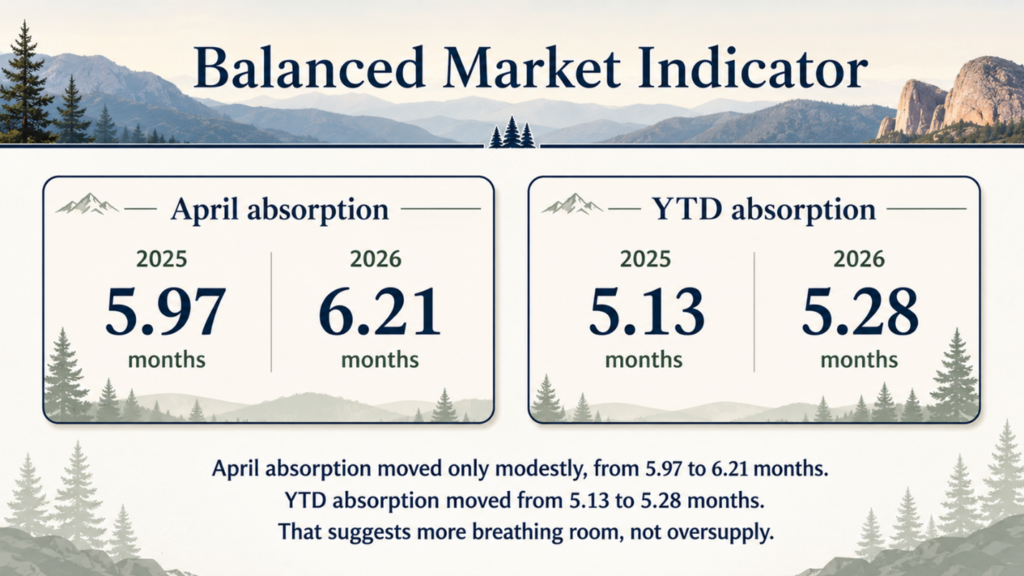

Absorption also supports the balanced-market interpretation. April absorption moved from 5.97 months last year to 6.21 months this year, while the year-to-date absorption rate moved only modestly, from 5.13 months to 5.28 months. That is not a dramatic oversupply signal. It is a sign that the market has more room to breathe.

Still, this is not an oversupplied market. Rim Country is different from many urban markets. Our communities are shaped by national forest, topography, infrastructure, water considerations, and limited opportunities for large-scale expansion. Those factors continue to support long-term stability.

Inventory has improved, but scarcity remains part of the larger Rim Country story.

For REALTORS®, the practical effect is simple: the listing conversation has changed. It is no longer enough to say, “Inventory is limited.” We also have to explain what the seller is competing against today, in their specific area, in their specific price range, and in their property’s specific condition category.

That is a very different conversation than the one many sellers remember from the fastest part of the market.

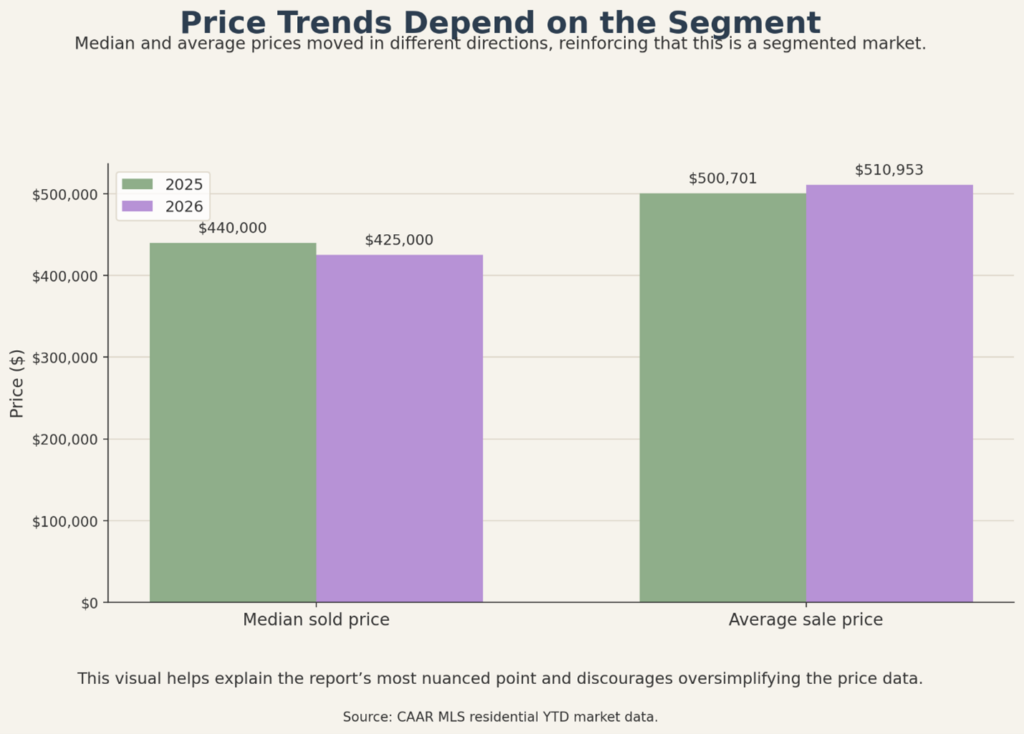

The pricing data requires careful interpretation.

The median residential sold price is down 3.41% year to date, while the average residential sale price is up 2.05%.

Those numbers are not inconsistent. They are a signal that this is a segmented market.

A lower median price does not automatically mean values are falling across the board. A higher average price does not automatically mean every seller has more pricing power. Together, those figures suggest a market being shaped by mix: which homes are selling, where they are located, what condition they are in, and which price bands are attracting the strongest demand.

That is why broad headlines can be misleading.

A cabin in Pine, a home in Payson, acreage in Young, a property in Happy Jack, and a second-home retreat near Christopher Creek may all be part of the broader Rim Country market, but they do not always move in the same way or at the same pace.

This continues the theme from our end-of-winter report. Rim Country is not a momentum-driven market anymore. It is a segmented, strategy-driven market where outcomes vary by price range, property condition, location, and execution.

For our members, this is one of the most important talking points of the season. Median price, average price, and sale-to-list ratios are useful, but they are not substitutes for market interpretation. We should be careful not to overstate appreciation, overstate softening, or treat regional averages as if they apply equally to every listing appointment.

The most valuable analysis is the one that answers the client’s actual question: what is happening in my segment of the market?

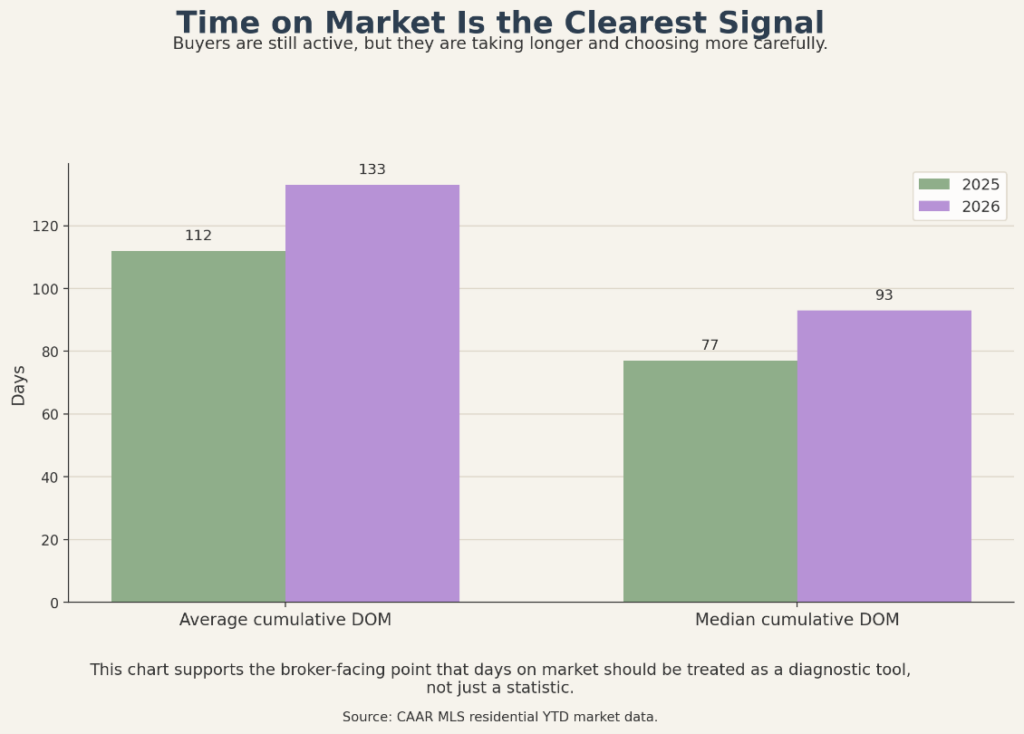

The clearest signal in the current data may not be price. It may be time.

Average cumulative days on market increased from 112 days to 133 days year to date. Median cumulative days on market increased from 77 days to 93 days.

That tells us buyers are taking longer to make decisions.

This does not mean they are absent. The increase in sold and pending activity shows they are still here. But it does mean they are more deliberate.

Homes that are priced correctly, prepared well, and marketed professionally are still attracting attention. Homes that are overpriced, underprepared, or difficult to compare against better-positioned alternatives are sitting longer.

That is the defining feature of this market. The spring market is not about speed. It is about strategy.

Absorption moved only modestly year over year, supporting the conclusion that Rim Country has more room to breathe, not a dramatic oversupply problem.

For brokers, this is also an important coaching point. Longer days on market can create frustration for agents and clients alike. The answer is not always a price reduction, but the answer is always a reassessment. Pricing, showing feedback, property condition, photography, access, buyer objections, competing inventory, and seller expectations all need to be reviewed together.

In a fast market, time on market can be overlooked. In this market, it is one of the most important diagnostic tools we have.

Condition is becoming one of the clearest dividing lines in the market.

Buyers are still willing to act, but they are more cautious about deferred maintenance, outdated systems, insurance issues, and properties that require immediate investment after closing. In this environment, preparation is not cosmetic. It is strategic.

That is especially true in a market like ours, where properties can vary significantly in age, construction type, access, slope, utility availability, heating and cooling systems, septic condition, roofing, defensible space, and maintenance history.

Rim Country buyers continue to value lifestyle, setting, and natural surroundings, but today’s market also places greater emphasis on condition, access, maintenance, and realistic pricing.

A buyer may still love Rim Country. A buyer may still want the lifestyle. But that does not mean the buyer will ignore obvious repair concerns, insurance uncertainty, or a price that does not reflect condition.

For REALTORS®, this means preparation advice matters. We should be encouraging sellers to look at their homes through the eyes of today’s buyer, not yesterday’s buyer. Presentation matters, but so does substance. Clean, accessible, well-documented, well-maintained properties have an advantage.

Higher-priced properties continue to play an important role in Rim Country.

Year to date, the $500,000-plus category accounted for 106 sold listings, up from 91 during the same period last year. Pending listings in that category increased from 93 to 117. Active listings in the $500,000-plus range also increased from 341 to 385.

That combination matters.

Higher-end buyers are still active, but they also have more choices. Sellers in this segment cannot rely on price point alone. Condition, setting, access, views, improvements, floor plan, privacy, and presentation all matter.

This is important because many Rim Country buyers are motivated by lifestyle, retirement planning, second-home use, remote work flexibility, or long-term relocation goals. Many are coming from markets where home equity remains substantial. Others are seeking a different quality of life and are willing to wait for the right property.

But the upper end is not automatic.

More inventory in higher price ranges means buyers have more room to compare. They may have resources, but they are still selective. They expect quality, condition, location, and value to align.

For listing agents, the upper-end market requires careful positioning. For buyer agents, it requires strong education about value, replacement cost, uniqueness, and scarcity. A higher price point does not eliminate the need for negotiation, due diligence, or market discipline.

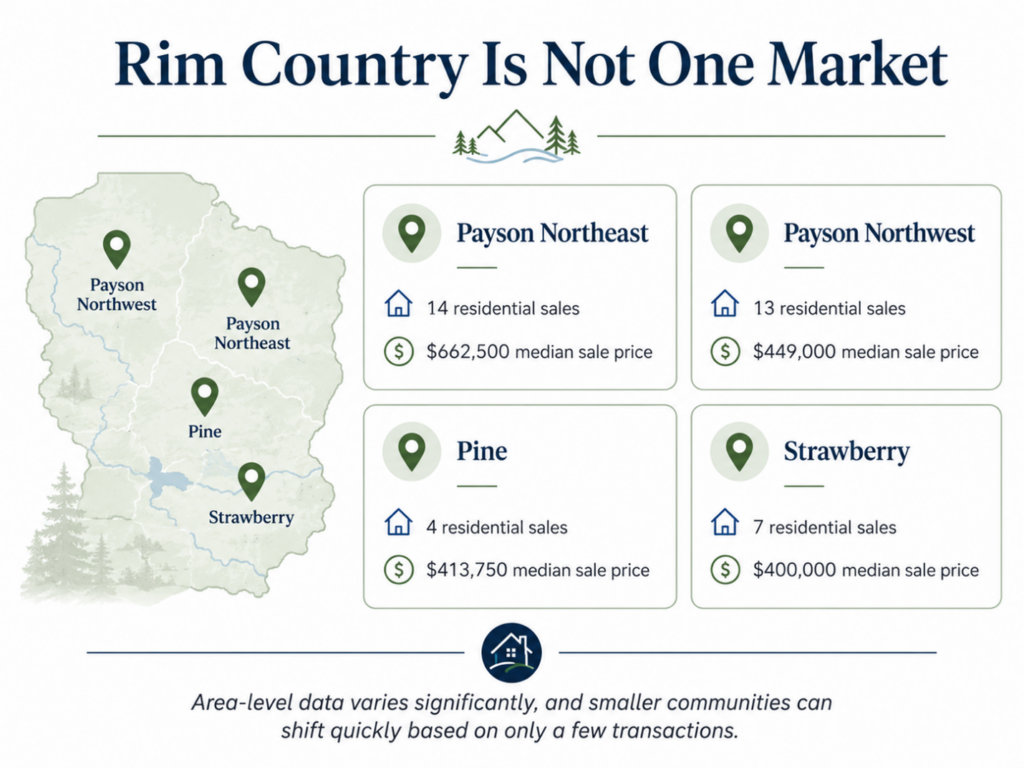

One of the most important responsibilities we have as REALTORS® is helping clients understand that Rim Country is not one uniform market.

Area-level data shows meaningful differences across communities. During the most recent reporting period, Payson Northeast recorded 14 residential sales with a median sale price of $662,500. Payson Northwest recorded 13 residential sales with a median sale price of $449,000. Pine recorded 4 residential sales with a median sale price of $413,750, while Strawberry recorded 7 residential sales with a median sale price of $400,000.

Recent-period area comparison, 4/24/2026 to 5/24/2026. Area-level residential data varies significantly, and smaller communities can shift quickly based on only a few transactions.

Source: CAAR MLS Sales Statistics by Area, 4/24/2026 to 5/24/2026.

Those differences matter.

In several Rim Country communities, a percentage change can look dramatic even when it reflects only a few additional transactions. In those markets, the transaction count and property mix often matter more than the percentage change.

In lower-volume communities, one or two transactions can significantly affect averages or median prices. A unique property, a luxury home, an acreage parcel, or a distressed listing can move the statistics in a way that does not reflect the entire market.

The better question is not simply, “What is the Rim Country market doing?”

The better question is, “What is this specific segment of the Rim Country market doing?”

That is where local expertise becomes essential.

For brokers and agents, this is also a reminder to be cautious with broad comparisons. A year-over-year percentage change in a small community can sound dramatic, but it may be driven by only a handful of transactions. In these situations, the actual number of sales, the type of properties sold, and the character of the inventory may be more meaningful than the percentage change itself.

Our clients rely on us to make those distinctions.

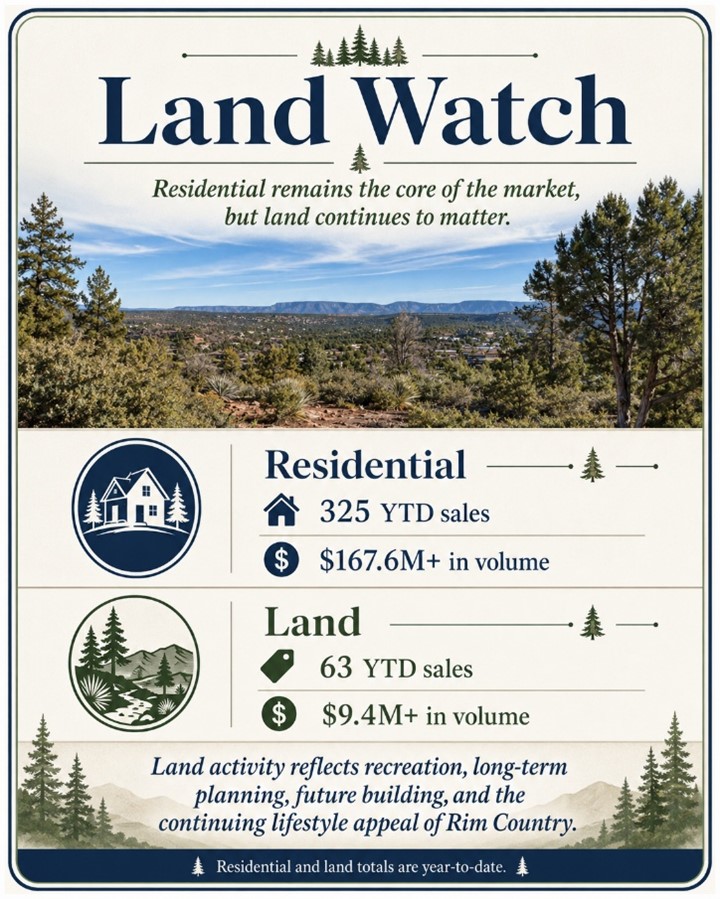

Residential sales remain the core of the CAAR market, but land activity continues to deserve attention.

The sales activity report shows 325 residential sales year to date, with residential volume of more than $167.6 million. Land sales accounted for 63 year-to-date sales and more than $9.4 million in volume.

Land Watch, year-to-date activity. Land remains a lifestyle and long-term planning category, but due diligence remains critical.

Source: CAAR MLS Sales Activity by Property Type Report, YTD 2026.

Land demand often reflects more than immediate housing activity. It can reflect future building plans, recreation, lifestyle decisions, long-term investment, and the continued appeal of owning a piece of Rim Country.

Some buyers view land as a longer-term path into the region. Others are drawn by the ability to create a custom retreat or hold property for future use.

Like residential property, land is highly location-specific. Access, utilities, zoning, topography, water, road conditions, and buildability all matter.

For REALTORS®, this is another area where professional guidance is critical. Land can be one of the most misunderstood property categories for consumers. A parcel may look attractive online, but the real analysis often involves access, utilities, septic feasibility, floodplain issues, easements, slope, zoning, permitting, water, and realistic development costs.

That makes land a lifestyle opportunity, but also a due diligence-heavy transaction.

For sellers, the message is clear.

The market is still producing strong results, but it is no longer forgiving aspirational pricing.

Sellers who price ahead of the market may find themselves chasing it later. Sellers who price within the market, prepare well, and respond to feedback are still seeing success.

A successful seller in this market should focus on four things.

The sellers who adjust to the current market are still finding success. The sellers who price based on yesterday’s momentum may face longer marketing times and more difficult negotiations.

For listing agents, this means the initial pricing conversation is more important than ever. It also means documentation matters. Sellers need to see the competition, understand days on market, and recognize how buyers are comparing their home to other available choices.

A good listing strategy today is not just about getting the property on the market. It is about entering the market correctly.

For buyers, the spring market offers opportunity.

There are more choices than there were during the tightest inventory periods. The pace is more reasonable. Buyers have more room to evaluate properties, compare options, and make thoughtful decisions.

But buyers should not mistake a more balanced market for a weak one.

Well-priced properties are still attracting attention. Desirable homes in strong locations can still move quickly. Buyers who are prepared, prequalified, and guided by local market knowledge remain in the strongest position.

The opportunity for buyers is not that every property is discounted.

The opportunity is that the market now allows for more careful decision-making.

For buyer agents, this means preparation still matters. Financing, proof of funds, realistic expectations, local market education, inspection strategy, and timely communication remain essential. A buyer who assumes the market has shifted entirely in their favor may lose a good property. A buyer who understands the difference between leverage and overreach will be better positioned.

This is a market where patience can help buyers, but hesitation can still cost them the right home.

For CAAR members, this is exactly the kind of market where professionalism matters most.

In a fast market, momentum can hide mistakes. In a balanced market, skill becomes visible.

Clients need help interpreting data. They need guidance on pricing, preparation, negotiation, financing, inspection issues, insurance considerations, and realistic timelines. They need us to explain why one segment may be moving quickly while another is slowing down. They need us to separate national headlines from local reality.

This is not a hype-based market.

This is a professional market.

For brokers, this is also a leadership moment. Agents need support in reading the data, communicating market shifts accurately, and setting client expectations early. The agents who succeed in this environment will be the ones who can explain not only what the numbers are, but what the numbers mean.

For consumers, broad headlines do not answer the most important questions. They do not tell a seller how to price a specific home in Pine, Payson, Strawberry, Happy Jack, Tonto Basin, or any other Rim Country community. They do not tell a buyer whether a property is positioned correctly, whether days on market reflect overpricing or property condition, or whether a particular segment is moving faster than the regional average.

That is where REALTORS® bring value: interpreting the data, understanding the local differences, and helping clients make informed decisions.

The REALTORS® who understand the data, communicate clearly, and guide clients with confidence will continue to stand out.

If I were summarizing this market for an office meeting, I would focus on five points.

Those are the conversations that will help agents provide better guidance and help clients make better decisions.

“The market is active, but buyers are more selective. The best-positioned homes are still moving, but pricing and condition matter more than they did during the fastest part of the market.”

“You have more room to compare than buyers had during the tightest inventory periods, but the best properties are still attracting attention. Preparation and realistic expectations still matter.”

“Rim Country remains resilient, but this is not a one-size-fits-all market. The right strategy depends on the property, the price range, the condition, and the specific community.”

The story of spring is not weakness. It is discipline.

Rim Country continues to benefit from lifestyle demand, limited land availability, long-term ownership, and the enduring appeal of our communities. But the market has changed. Buyers are more selective. Sellers face more competition. Outcomes increasingly depend on preparation, pricing, and professional execution.

That is why the role of a REALTOR® matters more, not less.

In a market driven by speed, momentum can carry the day. In a market driven by strategy, knowledge makes the difference.

This spring confirmed that Rim Country remains resilient. It also confirmed that success now belongs to those who understand the market clearly and respond to it wisely.

For buyers, that means preparation.

For sellers, that means realistic pricing and strong presentation.

For REALTORS®, that means leadership.

Rim Country continues to offer something that cannot be easily replicated: natural beauty, lifestyle, community, and long-term appeal. Those fundamentals remain strong.

But in today’s market, fundamentals must be matched with strategy.

Rim Country remains resilient. But in today’s market, resilience alone is not the story. The real story is how preparation, pricing, and professional guidance turn opportunity into results.

Interested in what CAAR does and how you can get involved? Contact us below to talk to our team.