New Federal Housing Law: What It Could Mean for Rim Country REALTORS®

By Central Arizona Association of REALTORS® President Dennis Riccio

A buyer may be prequalified. The unit may appraise. The inspection may be acceptable. The seller may be ready to close. But in a condo, townhome, patio home, or certain HOA-governed property, there is another question that can make or break the transaction:

Does the project itself qualify?

That question is becoming more important. Across the country, condominium and HOA-governed properties are receiving increased scrutiny because of insurance costs, reserve requirements, deferred maintenance, special assessments, investor concentration, rental concentration, and lender project-review rules.

Central Arizona is not Florida, Phoenix, Scottsdale, or Tucson. Our local condo inventory is limited, and our MLS category combines several different property types. But the same issues can still affect our transactions. In a smaller Central Arizona project, one investor, one insurance gap, one underfunded reserve account, or one unresolved maintenance issue can affect a much larger percentage of the project than it would in a large urban condominium community.

This is not an article claiming that Central Arizona is facing a condo crisis. It is a reminder that condos, townhomes, patio homes, and similar HOA-governed properties require a different due-diligence process than detached single-family homes.

Most CAAR members will not handle a large number of condo transactions each year. That is part of the risk. Because the segment is small, it can be easy to assume these transactions work like detached homes. They do not.

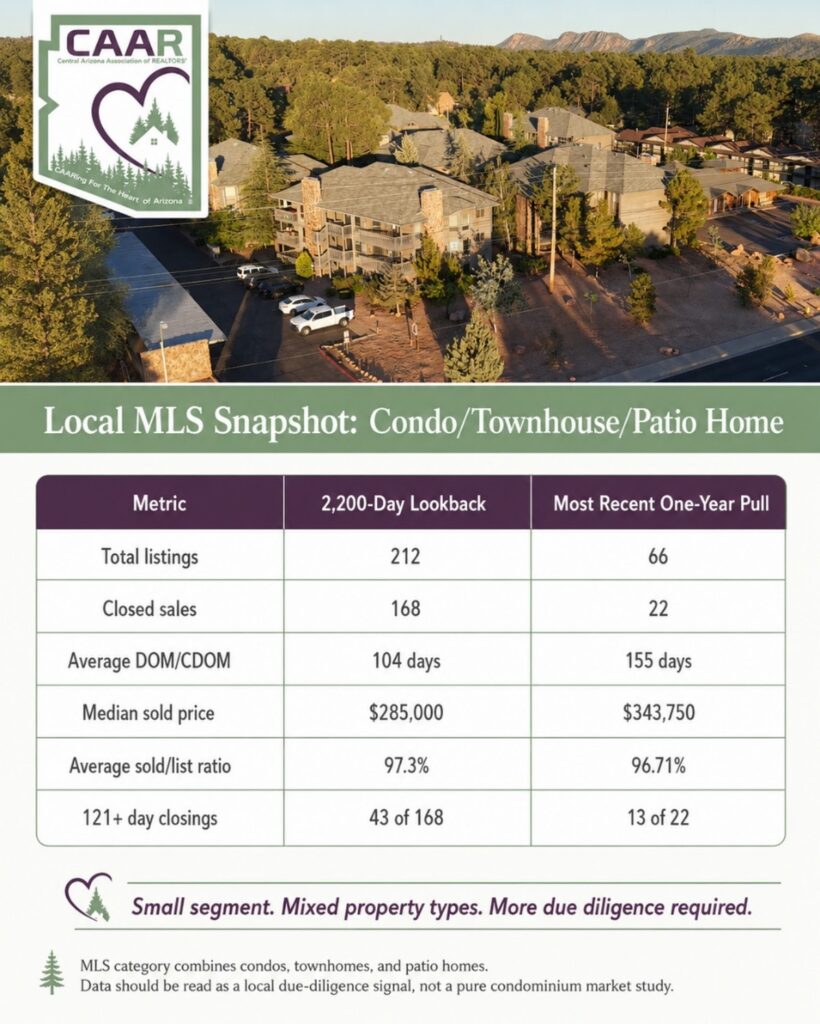

Recent one-year activity appears slower than the longer-term baseline, but the category is mixed and should be read as a due-diligence signal, not a pure condo-market study

This data should be read carefully. The MLS category is not a pure “condo” dataset. It includes condos, townhomes, and patio homes, and those ownership structures can have very different legal, insurance, maintenance, and financing implications. The data does not prove that Central Arizona has a condo-specific problem. But it does show that this is a small, specialized segment, and the most recent year appears slower than the longer-term baseline.

That makes due diligence more important, not less.

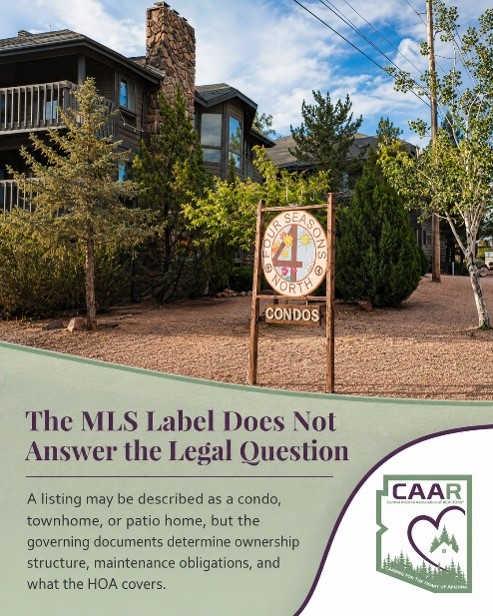

One of the challenges for agents is that the MLS property subtype does not answer every question that matters in the transaction.

A property may be listed as a condo, townhome, or patio home, but the important questions are more specific:

What is the legal ownership structure?

What do the CC&Rs say?

What does the HOA maintain?

What does the owner maintain?

What insurance does the association carry?

What does the lender require?

Are there reserves, special assessments, litigation, deferred maintenance, rental restrictions, or ownership-concentration issues?

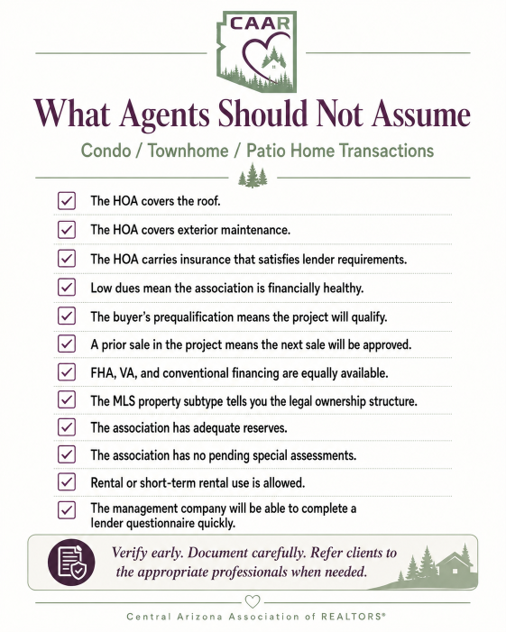

Those questions matter because one project may have the HOA responsible for roofs, exterior maintenance, insurance, trash, sewer, streets, or common elements. Another project may place many of those responsibilities on the individual owner. Some associations are professionally managed. Others are self-managed. Some have healthy reserves and good maintenance histories. Others may be working through deferred maintenance, insurance pressure, litigation, or governing-document limits on assessment increases.

The label gets us started. The documents give us the answer.

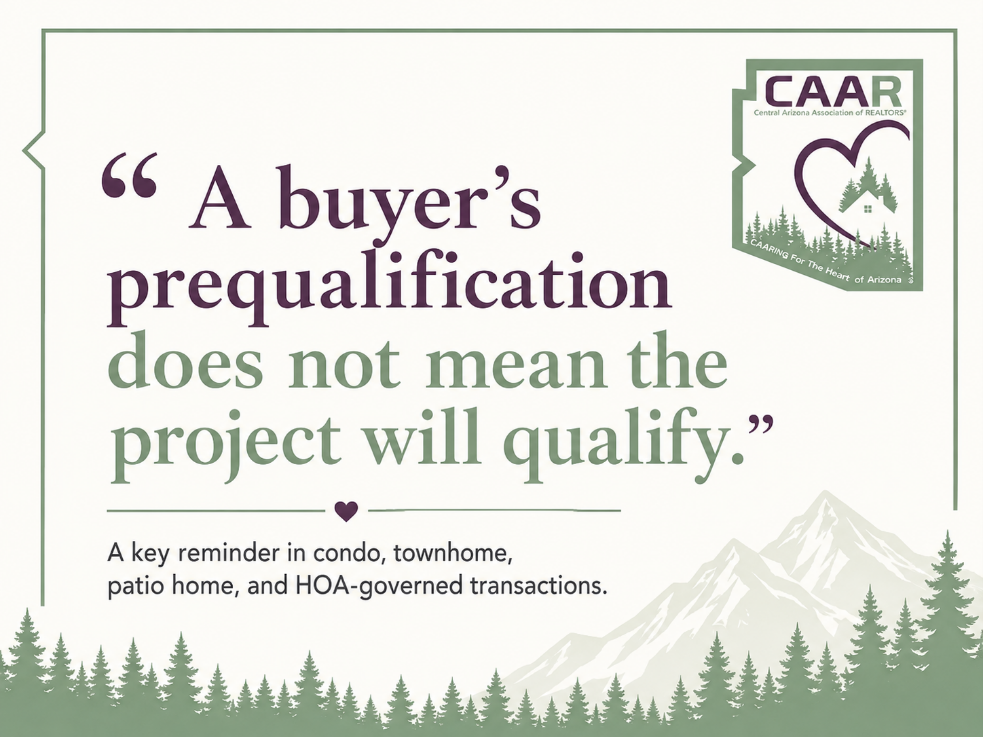

I recently spoke with Kevin Quame, a CAAR business partner and lender who works in the Payson market and has handled many recent condo-related lending issues in the Phoenix area. Kevin emphasized a point every REALTOR® and broker should remember: a buyer can be fully qualified, but the project itself may not be.

In a detached-home transaction, the lender primarily evaluates the borrower, the property, the appraisal, and the loan program. In a condominium or certain HOA-governed property, the lender may also evaluate the association and the project. That review can include issues such as single-entity ownership, investor concentration, rental concentration, master insurance coverage, fidelity or crime coverage, reserves, litigation, special assessments, and deferred maintenance.

Kevin identified single-entity ownership as a major issue, especially in smaller projects. If one person, company, investor group, trust, LLC, or related ownership group owns too many units, the project may become ineligible for certain conventional financing. In small projects, that threshold can be reached quickly. For a 5-to-20-unit project, ownership of more than two units by one entity may create a problem. In a small Payson-area complex, one investor can therefore affect the financing options for the entire project.

Kevin also explained that agents and buyers may not know whether a project will satisfy lender requirements until the property is under contract and the lender begins project review. If the project is flagged, the lender may require a condo questionnaire or additional HOA documents. That process can take time. If the association cannot provide the information, or if the answers reveal an insurance, reserve, ownership, rental, or maintenance issue, the transaction can be delayed or fail.

That means listing agents should be careful before advertising broad financing availability in the MLS. If a listing says conventional, FHA, VA, or other financing is available, the listing side should have a reasonable basis for that representation.

Insurance has become one of the biggest issues affecting condos and HOA-governed properties nationally. Rising premiums, higher deductibles, and reduced coverage can affect more than monthly dues. They can affect whether a buyer can finance the property.

If an association reduces coverage to control costs, the project may no longer meet lender guidelines. Some associations may attempt to reduce or remove certain types of coverage to manage premiums. That may save money in the short term, but it can create problems if the lender determines that the master policy is inadequate.

In mountain communities like ours, insurance questions may become even more important. Wildfire exposure, roof age, maintenance history, claims history, deductible levels, and fire-hardening requirements can all affect insurance availability and cost. Even where coverage remains available, premiums can change quickly. When the only real source of HOA revenue is the owners, rising insurance costs eventually show up somewhere: higher dues, reduced services, deferred maintenance, reserve pressure, or special assessments.

For REALTORS®, the takeaway is simple: do not treat insurance as an afterthought. Ask early for the master insurance certificate, deductible information, and any recent history of premium increases or coverage changes.

I also spoke with Melissa Glinzak, CAAM, MBA, Executive Vice President of Northern Arizona Operations for Ogden & Company, Inc., which manages HOA communities in the Payson area. Melissa’s practical advice was straightforward: every project is different.

That may be the most important point in this discussion.

Melissa emphasized that agents should not assume what the HOA covers. In some communities, the HOA may cover exterior maintenance, roofs, trash, sewer, common areas, or insurance. In other communities, the owner may be responsible for items that buyers often assume are covered by the association. Some communities may have transfer fees, capital contribution fees, working capital fees, prepaid assessments, rental restrictions, short-term rental restrictions, or governing-document limitations on assessment increases.

Her recommendation was simple: read the CC&Rs, review the association documents, and call the management company when there is a question.

That advice is especially important in our market because many of these properties are older, smaller, or part of unique local developments. In some cases, associations may have been self-managed for years. In some cases, dues may have been kept low because no one wanted to raise assessments on neighbors. That can make a property look affordable on paper, but it may also mean reserves are thin or maintenance has been deferred.

Low dues are not always a sign of a healthy association. Sometimes they are a sign that the hard decisions have been postponed.

Before listing a condo, townhome, patio home, or similar HOA-governed property, listing agents should consider the following:

Before writing an offer on a condo, townhome, patio home, or similar HOA-governed property, buyer’s agents should consider the following:

These questions are not designed to discourage buyers. They are designed to avoid surprises.

For brokers, this is also a supervision and risk-management issue.

If an MLS listing advertises conventional, FHA, VA, or other financing, the listing side should have a reasonable basis for that representation. If an agent tells a buyer that the HOA covers the roof, exterior maintenance, insurance, trash, sewer, or certain utilities, that statement should be grounded in the governing documents or confirmed by the association or management company.

If a buyer is told that rentals or short-term rentals are allowed, that should be verified. If a buyer is told that the association is responsible for a particular repair, that should be verified. If a buyer is relying on FHA, VA, or conventional financing, project eligibility should be addressed early.

Brokers may want to discuss this issue at office meetings and encourage agents to develop a standard document-request and lender-verification process for condo, townhome, patio-home, and HOA-governed listings.

Our role is not to guarantee the financial health of an association or provide legal, lending, insurance, or accounting advice. But we can ask better questions, avoid unsupported assumptions, and direct clients to the right professionals.

Central Arizona is not a large condominium market. We do not have the density or volume of Phoenix, Scottsdale, Tucson, or Florida. But we do have condos, townhomes, patio homes, and HOA-governed properties. Some are attractive options for buyers seeking lower exterior-maintenance obligations, lock-and-leave convenience, second-home use, or a different price point than detached single-family homes.

The lesson is not that buyers should avoid these properties. The lesson is that these transactions require a different set of questions.

For CAAR members, the best practice is simple: ask earlier, verify more, and avoid assumptions.

In this segment of the market, due diligence is not just about the unit. It is about the association behind it.

This article is intended for general education and risk awareness only. REALTORS® should encourage clients to consult their lender, insurance professional, attorney, CPA, HOA manager, and other appropriate professionals regarding specific transaction issues.

Interested in what CAAR does and how you can get involved? Contact us below to talk to our team.