Wildfire Preparedness and Insurance Are Now Closing Issues in Rim Country

As insurance underwriting changes in wildfire-prone areas, CAAR members are being encouraged to address mitigation, defensible space, and insurance availability earlier in the transaction.

By Dennis R. Riccio

President, Central Arizona Association of REALTORS®

July 2026

CAAR members gathered for the July Business Breakfast to discuss wildfire preparedness, insurance availability, and legislative issues affecting Rim Country real estate.

Wildfire preparedness is no longer just a safety issue in Rim Country. It is now directly tied to insurability, buyer confidence, seller preparation, and the ability to close a transaction on time.

At CAAR’s July Business Breakfast, members heard from Kevin McCully with the Payson Fire Department and Eric Santana with State Farm Insurance about wildfire behavior, home hardening, evacuation planning, and the changing insurance environment in wildfire-prone communities. Clark Jones also provided a legislative update, including recent REALTOR® advocacy involving insurance underwriting transparency.

The message for REALTORS® was clear: fire mitigation and insurance availability need to be part of the real estate conversation early, especially in Payson, Pine, Strawberry, Bonita Creek, Washington Park, Chaparral Pines, The Rim Golf Club, and other forest-interface communities.

Kevin McCully explained that wildfires often do not move through neighborhoods as a single wall of flame. Instead, embers can ignite vegetation, bark mulch, fences, firewood, patio items, or other combustible materials near a structure. Once one home catches fire, the structure itself becomes fuel, and the fire can move from house to house. That type of structure-to-structure spread is known as a conflagration.

Kevin compared large urban fire events with Rim Country’s local realities. Larger agencies may have the ability to place multiple engines on a single street during a fire event. Rim Country does not have that same level of resources. Local fire departments must make strategic decisions about where they can safely and effectively deploy personnel and equipment.

That makes individual homeowner preparation especially important. A mitigated property is not only safer for the home. It may also be a property where firefighters have a better chance of working safely and successfully.

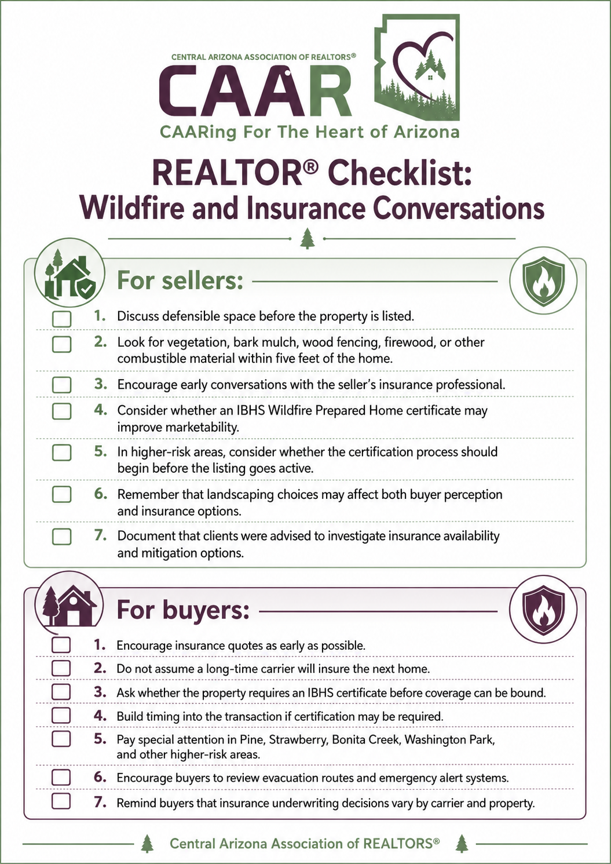

The presentation emphasized practical steps homeowners can take, including keeping combustible materials away from the first five feet around the home.

One of the most important takeaways from the presentation was the importance of the first five feet around a home.

That immediate zone should be kept free of combustible materials. In plain terms, homeowners should avoid bark mulch, shrubs, firewood, combustible patio items, artificial turf, and wood fencing attached directly to the structure within that five-foot area. Noncombustible materials such as gravel, concrete, pavers, or similar surfaces are preferred.

Kevin discussed research from the Insurance Institute for Business & Home Safety, commonly referred to as IBHS. IBHS studies how homes ignite during wildfire events, including how embers interact with structures and surrounding materials. The research supports what fire professionals have long emphasized: relatively simple changes around a home can significantly reduce wildfire vulnerability.

This does not mean every tree needs to be removed. Kevin explained that trees can often remain if they are properly maintained, trimmed away from the home, and the leaf litter and ladder fuels underneath them are removed. The more immediate concern is combustible material that allows fire to creep directly into the structure.

Wildfire preparedness is not limited to landscaping. It also includes evacuation planning.

Kevin McCully with the Payson Fire Department discussed wildfire behavior, defensible space, evacuation planning, and the importance of mitigation around homes.

Kevin encouraged residents to identify more than one way out of their neighborhood and more than one way to reach the main routes out of town. He recommended that residents physically drive those routes instead of simply looking at a map. In an emergency, the usual route may be blocked, congested, or unsafe.

This is especially important in older neighborhoods that may have limited ingress and egress. Some communities were built before modern secondary-access requirements. Newer communities may be required to have a second exit once they exceed certain size thresholds, but older areas cannot always be retroactively redesigned.

Kevin also emphasized that residents should not wait for someone to knock on the door before leaving. If ash is falling, conditions feel unsafe, or an area is placed on “set” status, residents can leave early. Early evacuation can reduce congestion, help emergency responders get into threatened areas, and give residents more control over their own safety.

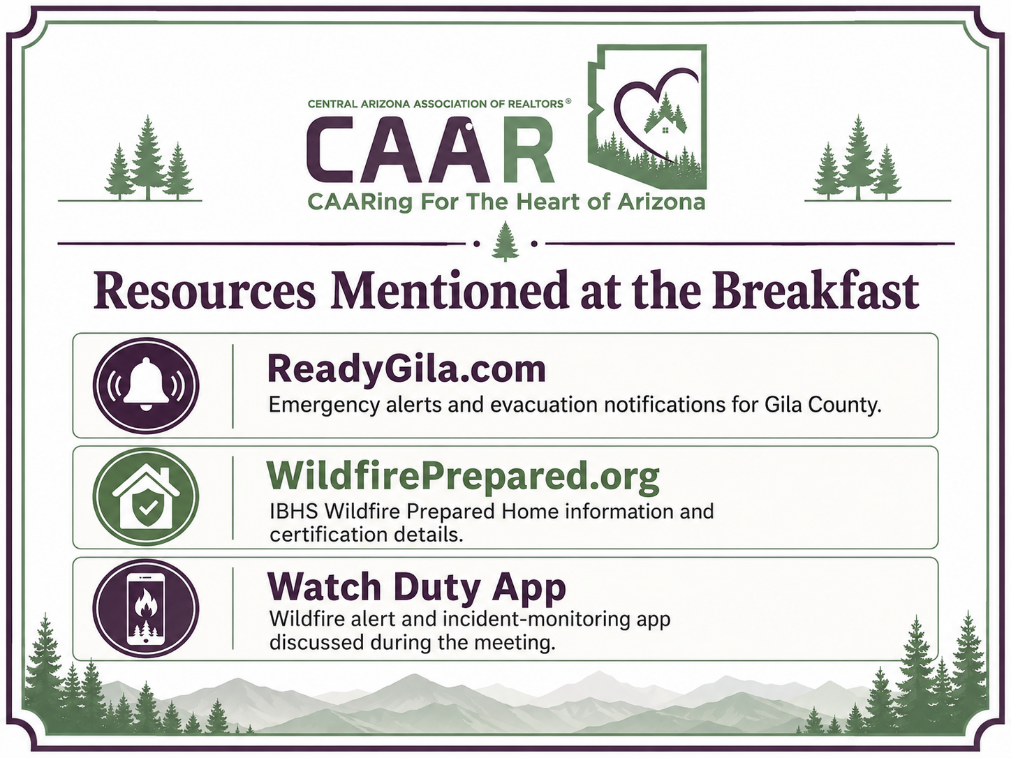

Members were reminded of ReadyGila.com as a key resource for emergency alerts, evacuation notices, and special assistance information for residents who may need help evacuating.

The breakfast also included updates on insurance challenges, underwriting concerns, and REALTOR® advocacy affecting property owners in wildfire-prone areas.

Eric Santana then addressed the insurance side of the issue. His remarks made clear that wildfire risk is now directly affecting whether certain homes can be insured, how quickly insurance can be obtained, and what buyers and sellers may need to do during a transaction.

Eric explained that State Farm implemented a new property-screening system beginning May 15. When a buyer or homeowner seeks coverage, the property is run through the system to determine whether State Farm can insure it, whether an IBHS Wildfire Prepared Home certificate is required, or whether the property is not currently eligible for coverage through State Farm.

One of the most memorable examples was Eric’s own home. He explained that if he sold his house today, State Farm would not insure it under the current system because of its location and surrounding wildfire risk. That example showed members that this issue is not theoretical. It is already affecting properties in our market.

Eric also noted that some properties in Payson may proceed normally, many may require an IBHS certificate, and some may not currently be eligible through State Farm. In Pine, Strawberry, Bonita Creek, Washington Park, and other higher-risk areas, coverage may be even more difficult to obtain.

For REALTORS®, one of the most important practical points is timing.

Eric explained that obtaining an IBHS Wildfire Prepared Home certificate can take approximately 30 to 45 days. The homeowner must go through the Wildfire Prepared Home process, complete the checklist, submit photos and documentation, pay the certificate fee, and, if the property appears to qualify, have the property reviewed before the certificate is issued.

That timing matters because many escrows are also approximately 30 to 45 days. If a buyer waits until after contract acceptance to begin the insurance process, and the property requires an IBHS certificate before an application can even be submitted, insurance can quickly become a closing issue.

For sellers in wildfire-prone areas, mitigation and certification may be worth considering before the home goes active. For buyers, insurance availability should be checked as early as possible, preferably before making an offer or immediately after contract acceptance.

Eric also clarified an important point about the IBHS program. There are different levels of recognition, including a higher “Plus” standard. Some homeowners may see the “Plus” requirements and assume they need to replace siding, roofing, or other major building components.

For many current underwriting purposes, Eric indicated that the basic certificate is the key requirement. The basic focus is wildfire preparation, especially the noncombustible five-foot zone around the home, vegetation management, and reducing ignition risks near the structure.

That distinction matters. Homeowners may be more willing to take action if they understand that the first step may be focused on practical mitigation rather than major reconstruction.

Save this member resource: The following CAAR-branded checklist summarizes the key wildfire, insurance, and preparedness conversations REALTORS® may want to have with sellers and buyers early in the transaction.

This CAAR member resource summarizes seller and buyer conversation points, key resources, and the main transaction takeaway from the July Business Breakfast.

Clark Jones concluded with a brief legislative update, including REALTOR® advocacy at the national and state levels.

One item directly related to the breakfast topic was Arizona House Bill 2174, which Clark described as addressing how insurance companies use third-party information in underwriting and premium adjustments. The concern is that inaccurate mapping or third-party data can affect whether homes are insurable or how premiums are calculated.

Clark explained that REALTOR® advocacy is focused on improving accuracy and transparency so that property owners, REALTORS®, and insurance professionals have a clearer understanding of the information being used in underwriting decisions.

That issue is especially important in Rim Country, where wildfire risk, vegetation, topography, and mapping data can all affect real estate transactions.

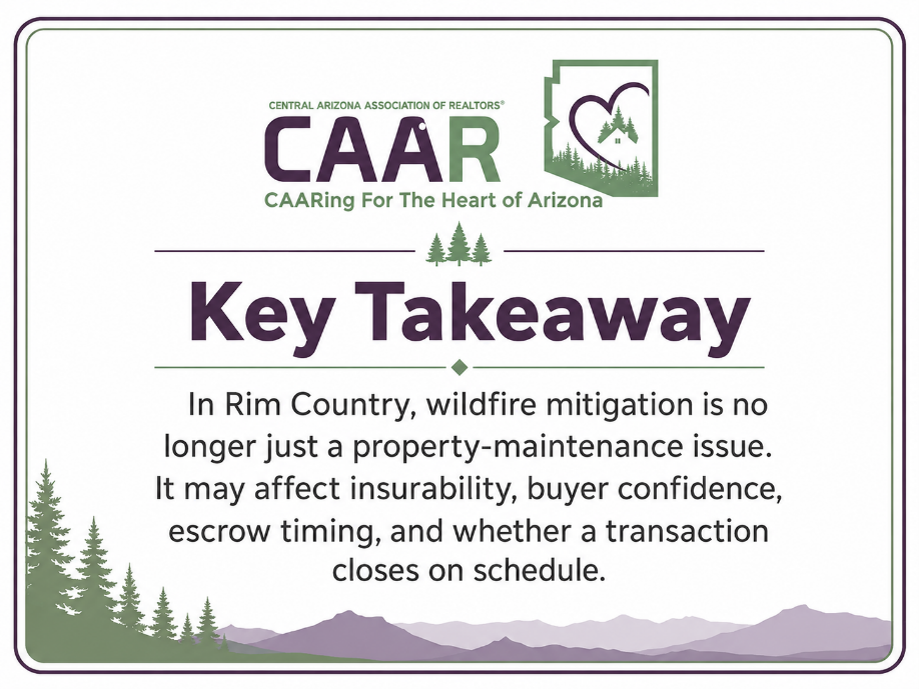

The practical takeaway is simple: wildfire preparedness and insurance availability are now part of the real estate transaction in Rim Country.

For sellers, this may mean preparing the property before going on the market. For buyers, it means investigating insurance early. For REALTORS®, it means helping clients understand that defensible space, the first five feet around a home, evacuation planning, and insurance underwriting can all affect marketability and closing timelines.

This article is intended for general education. Insurance underwriting decisions vary by carrier and property, and clients should speak directly with their insurance professional.

Wildfire risk is part of living in Rim Country, but the goal is not to scare people. The goal is to help homeowners prepare. The best time to address wildfire and insurance issues is before the listing goes live or before the buyer is deep into escrow.

In Rim Country, fire mitigation is no longer just good stewardship. It may be part of getting the home insured, sold, and closed.

This article is provided for general education for CAAR members. Insurance underwriting decisions vary by carrier and property. Clients should speak directly with their insurance professional regarding coverage options and requirements.

Interested in what CAAR does and how you can get involved? Contact us below to talk to our team.