Rim Country Short-Term Rental Market Update

By Dennis Riccio

President, Central Arizona Association of REALTORS®

March CAAR Business Breakfast Recap

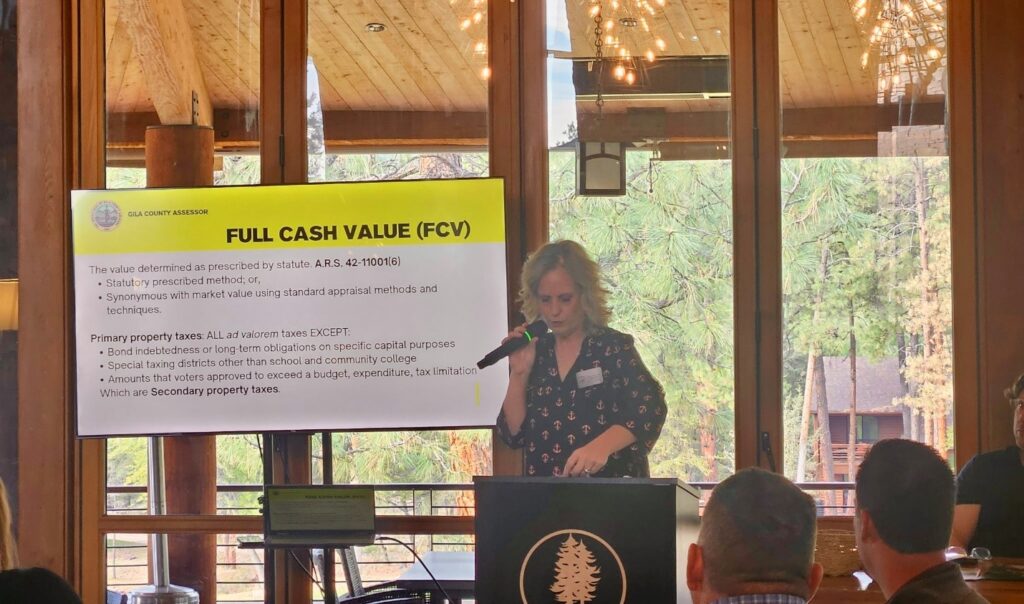

Members gather at Chaparral Pines Country Club for the March CAAR Business Breakfast featuring Gila County Assessor Sherra J. Kissee.

Speaker: Sherra J. Kissee, Gila County Assessor

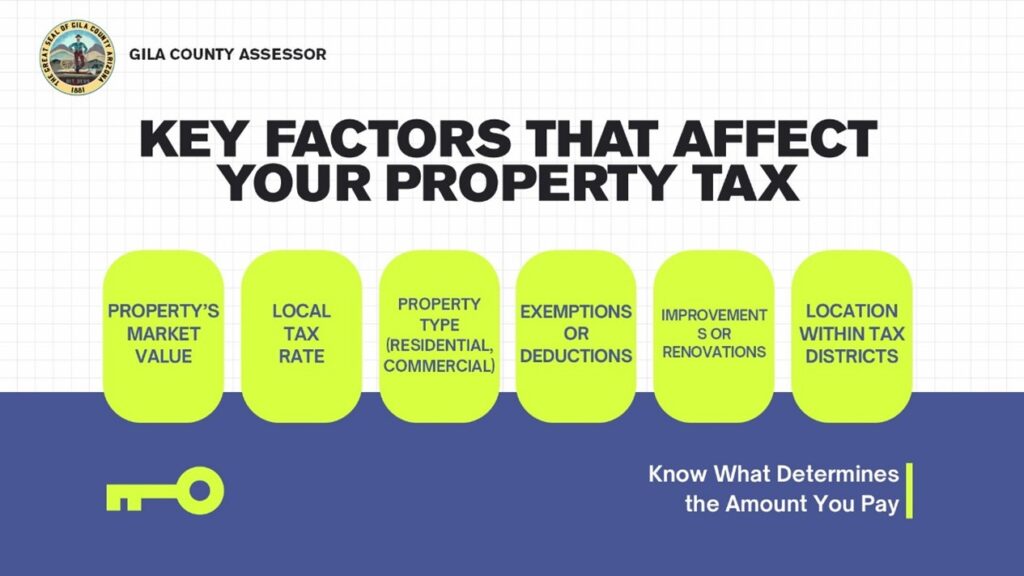

Property taxes are one of the most common questions REALTORS® receive from buyers and sellers. At our March 4 CAAR Business Breakfast, Gila County Assessor Sherra J. Kissee helped shed light on how Arizona’s property tax system actually works and why assessed values often differ from market prices.

A Record Turnout for the CAAR Business Breakfast

Our March 4 CAAR Business Breakfast was one for the books. This was the first time we held the event at the Chaparral Pines Country Club Restaurant, and the turnout exceeded anything we have seen in the past. Typically, our breakfast attendance ranges from 40 to 50 members. This time we had 65 people registered and even ended up with a waiting list, unfortunately having to turn a few people away once we reached capacity.

The response shows how valuable these gatherings are for our members. There were excellent networking opportunities, with many REALTORS®, brokers, and business partners in attendance. The Chaparral Pines staff did an outstanding job, and the food and service were excellent. We plan to continue using this venue and are already working on adding additional television monitors at future breakfasts so everyone in the room can easily see the presentation materials.

One important reminder for members is to please RSVP early. Chaparral Pines can accommodate more than 65 people for our events, but once we get within about a week of the breakfast we must provide final numbers and the event becomes capped. If demand continues like this, we hope to expand capacity so even more members can participate.

Our featured speaker for the March breakfast was Gila County Assessor Sherra J. Kissee, who provided an excellent overview of how property taxes are determined and how the assessor’s office operates. For REALTORS® and brokers who regularly answer client questions about property taxes, the information was extremely useful.

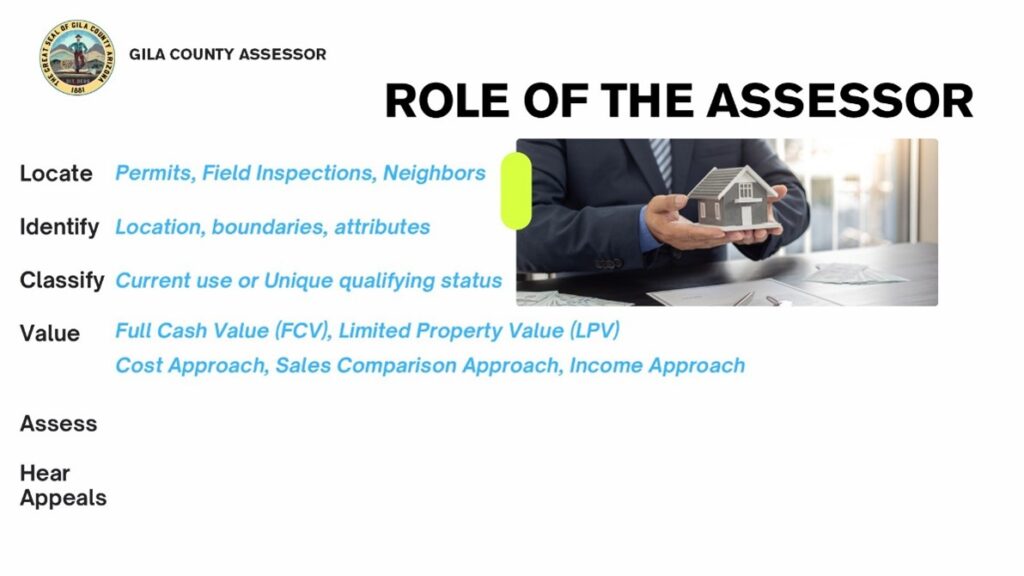

Many property owners assume the assessor’s office simply assigns a value to a property each year. In reality, the process is much more complex. As Kissee explained, “Our job is to locate, identify, classify, value, and assess every property in the county.”

Locating property means tracking changes through building permits, field inspections, and neighborhood reviews. Appraisers verify improvements such as additions, garages, sheds, and other structures that may affect valuation.

Identification involves confirming parcel boundaries, attributes, and location within specific districts. Classification determines how a property is categorized under Arizona law, such as a primary residence or commercial property. Arizona assessors must classify property based on current use, not “highest and best use,” which is commonly used in private sector appraisals.

Understanding Full Cash Value vs. Limited Property Value

How Property Taxes Are Calculated

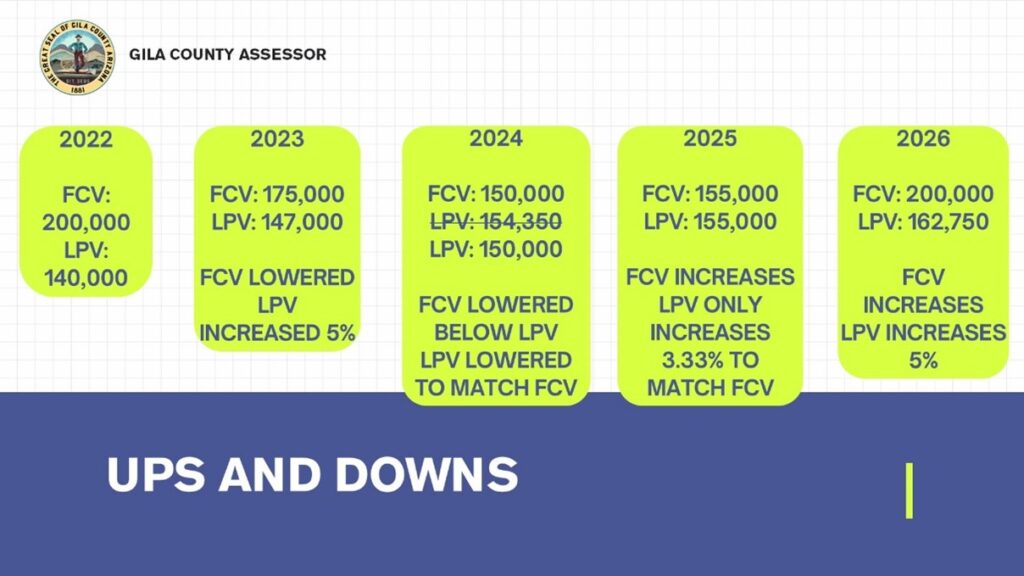

One of the most helpful parts of the presentation was the explanation of the difference between Full Cash Value (FCV) and Limited Property Value (LPV). Full Cash Value is essentially the statutory equivalent of market value determined through standard appraisal methods. Limited Property Value is the number typically used to calculate property taxes.

Arizona voters approved Proposition 117 in 2013, which limits annual increases in Limited Property Value to five percent in most situations. This means that even when market values fluctuate significantly, the taxable value used for property tax calculations increases gradually over time.

Example of how Limited Property Value changes differently from market value under Proposition 117.

“Arizona is not California. When a property sells here, the taxable value does not reset to the purchase price.”

— Gila County Assessor Sherra J. Kissee

This is also why Arizona property taxes behave differently than those in some other states. As Kissee noted during the presentation, “Arizona is not California. When a property sells here, the taxable value does not reset to the purchase price.” Instead, the Limited Property Value generally continues with the same annual adjustment unless substantial changes are made to the property. Instead, the Limited Property Value generally continues with the same annual adjustment unless substantial changes are made to the property.

From a REALTOR® perspective, understanding these concepts helps us answer many of the tax questions that come up during transactions. Buyers are often surprised to learn that property taxes in Arizona do not reset to the purchase price. Knowing how Limited Property Value works allows REALTORS® to explain why a home’s tax bill may not match the sale price or current market value.

Kissee also reviewed the three approaches used to determine Full Cash Value: the cost approach, which estimates replacement cost minus depreciation; the income approach, used for income-producing properties; and the sales comparison approach, which analyzes comparable sales and is the most common method used for residential property.

To maintain fairness and uniformity, the assessor’s office conducts a sales ratio study each year. This analysis reviews property sales to determine which transactions represent true arm’s-length market activity. Sales involving unusual circumstances such as family transfers, government acquisitions, or distressed sales may be excluded.

The time frame used in these studies is also important. For example, the current valuation cycle relied on sales from 2022 through 2024. This sometimes creates confusion when property owners point to a recent sale that falls outside the analysis period used for assessments.

Exemptions and Programs That Can Reduce Property Taxes

Another key topic was exemptions and programs that can reduce property taxes. Arizona offers exemptions for qualifying disabled veterans, widows or widowers, and individuals with total and permanent disabilities. In some cases, these exemptions can significantly reduce taxes or eliminate them entirely.

Seniors age 65 and older may also qualify for a “senior freeze,” which freezes the Limited Property Value so it does not continue increasing each year, provided ownership, residency, and income requirements are met.

Assessor Kissee also highlighted several common mistakes property owners make, such as ignoring the annual Notice of Value, failing to claim available exemptions, or not updating assessor records after property improvements. These issues can lead to incorrect records or missed opportunities to reduce property taxes.

She emphasized that property owners should review their Notice of Value carefully. “You can appeal your full cash value or classification,” Kissee explained, “but you cannot appeal the tax bill itself.”

The discussion also touched on an issue many REALTORS® encounter during property research: manufactured homes that were historically reclassified as site-built homes. The assessor’s office is currently working through the process of correcting some of those records, which will help improve data accuracy in the future.

I appreciate Assessor Kissee taking the time to speak with our members and share her expertise. Events like these demonstrate the value of staying engaged with your association and with the local officials who shape the environment in which we work.

Thank you to everyone who attended the March breakfast. With the level of participation we saw this month, it is clear these events continue to provide tremendous value to our membership. We look forward to seeing even more of you at our upcoming CAAR Business Breakfast events.

Several factors combine to determine a property’s tax bill.

Key REALTOR® Takeaways

Interested in what CAAR does and how you can get involved? Contact us below to talk to our team.