Rim Country Short-Term Rental Market Update

From the Desk of Dennis R. Riccio, President

President’s Message

As we transition out of winter and prepare for the spring market, one thing is clear. The Rim Country market is no longer being driven by momentum alone. It is being shaped by strategy, patience, and professionalism.

Over the past several years, many transactions were dictated by speed. Today, we are seeing a return to fundamentals. Pricing matters. Presentation matters. Negotiation matters.

This is not a declining market. It is a maturing one.

For CAAR members, this shift represents opportunity. The agents who understand the data and can clearly communicate it to their clients will be the ones who stand out in 2026.

Longer market times and increased inventory are shifting outcomes toward pricing accuracy and negotiation.

The broader Rim Country market reflects a clear rebalancing.

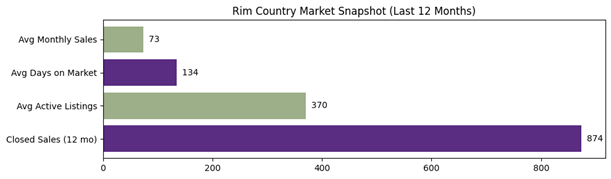

Key Insight: Nearly 75% of all listings are closed transactions, but marketing time has expanded significantly, signaling a shift away from urgency.

The data shows that while pricing remains relatively stable, the path to closing has lengthened. Buyers are taking more time, and sellers are facing more competition.

“The average days on market is approximately 134 days, with nearly 19% of listings taking more than four months to sell.”

This is critical. The longer a property sits, the more pricing pressure it faces. This is where REALTOR® expertise becomes essential.

Approximately 26% of listings are not resulting in a closed sale, reinforcing the importance of accurate pricing, preparation, and strategic marketing.

Key takeaway:

➡️ Roughly 1 in 4 listings are not closing and fall into expired/cancelled/off-market categories.

Higher-end sales are driving median price increases, not uniform appreciation across all price segments.

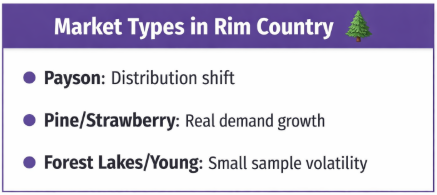

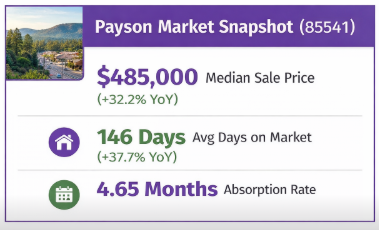

Payson remains the foundation of the Rim Country market and continues to show resilience in pricing.

At first glance, a 32% increase in median sale price suggests strong appreciation. However, this figure requires context to be properly understood. While the increase is mathematically accurate, it is not solely the result of uniform price growth across the market.

Instead, the data indicates that much of this increase is being driven by a shift in the mix of homes selling.

Specifically:

This type of shift can significantly raise the median price, even if individual home values are not increasing at the same rate across all segments.

Additional metrics reinforce this interpretation:

At the same time:

This creates a clear pattern:

Together, these indicators point to a distribution shift, rather than broad-based appreciation.

This is a more nuanced and selective market than the headline numbers suggest.

In practical terms:

The reported +32% increase in median price is real, but it should not be interpreted as uniform appreciation across the entire Payson market.

Instead, it reflects a shift toward higher-priced transactions within a lower-volume environment.

This reinforces a key theme across Rim Country:

This is no longer a momentum-driven market. It is a segmented, strategy-driven market where outcomes vary significantly by price range, positioning, and execution. Entry-level and mid-range inventory has softened, while higher-end homes (500K+) continue to carry the bulk of transaction volume.

Rising sales and pending activity reflect real demand, but percentage gains are amplified by low transaction volume.

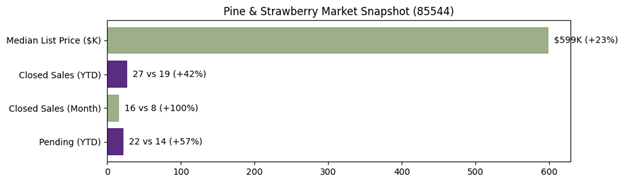

This area continues to show strong demand, particularly for lifestyle and second-home buyers, but activity levels should be interpreted within the context of a smaller market.

Strong Demand, Small Market

🟣 $599,000

Median List Price

(+23% YoY)

🟢 22 vs 14

Pending Sales (YTD)

(+57%)

🟣 16 vs 8

Closed Sales (Month)

(+100%)

🟢 27 vs 19

Closed Sales (YTD)

(+42%)

“Pending activity is significantly outpacing prior year levels, even as pricing becomes more sensitive.”

Key Insight: Strong Growth, but from a Small Base

While percentage increases appear significant, they are driven by relatively small changes in total transaction count.

🟣 Market Reality Check

Growth is real, but driven by small numbers.

+100% sales increase = 16 vs 8 transactions

For example:

This confirms that:

What This Means

This market is behaving differently than Payson and reflects active, demand-driven conditions rather than statistical distortion.

Unlike larger markets:

Pine and Strawberry is best characterized as a high-demand, low-volume market, where growth is real, but percentages must be interpreted alongside actual transaction counts.

Home values remain steady, but extended days on market signal reduced urgency and increased buyer discretion.

Happy Jack reflects a classic normalization pattern.

Slower Pace, Stable Pricing

🟣 $594,000

Median Sale Price

(Stable YoY)

🟢 154 Days

Avg Days on Market

(+67% YoY)

🟣 4.94 Months

Absorption Rate

🟢 Inventory Increasing

Longer marketing times

🟣 Market Insight

This is a time-driven shift, not a price-driven decline.

Homes are taking longer to sell, but values are holding.

Key Insight: Time Expansion, Not Price Decline

At first glance, the increase in days on market could suggest a weakening market. However, pricing data tells a different story.

This indicates that:

What This Means

Happy Jack is transitioning from a speed-driven market to a time-driven market.

This creates a clear dynamic:

This is a market where patience has replaced urgency. Success depends less on chasing price and more on setting expectations around timing and positioning.

Market metrics are driven by just a few listings, making year-over-year changes highly sensitive to small shifts.

Forest Lakes continues to operate as one of the most constrained and lowest-volume markets in Rim Country, where even small changes in inventory or activity can create large percentage swings.

Extremely Limited Inventory, High Variability

🟣 $1,599,950

Median List Price

(-27.27% YoY)

🟢 2 vs 1

Active Listings

(+100%)

🟣 2.4 vs 1.0 Months

Absorption Rate

(+140% YoY)

🟢 0 vs 0

Closed Sales

🟣 Market Insight

This is an ultra-low volume market.

A single listing can significantly impact pricing and inventory metrics.

Forest Lakes is a very small sample market, where:

This means:

This is not a market where traditional year-over-year comparisons provide reliable trend signals.

Instead:

Forest Lakes should be viewed as a low-liquidity market, where percentage changes are less meaningful than actual transaction counts and individual property dynamics.

Fewer transactions, but well-priced homes are selling more quickly, indicating focused and disciplined buyer activity.

Tonto Basin showed one of the most interesting trends in the region.

Selective Demand, Efficient Closings

🟣 $356,000

Median Sale Price

(+14.29% YoY)

🟢 129 Days

Avg Days on Market

(-38.86% YoY)

🟣 Sales Volume ↓

Down 33% (MoM)

🟢 Faster Absorption

Well-priced homes moving quicker

🟣 Market Insight

Fewer buyers, but more decisive ones.

Demand exists, but only for correctly priced properties.

At first glance, the decline in sales volume may suggest weakening demand. However, the data indicates a more nuanced shift.

This combination reflects a market where:

Tonto Basin is not experiencing a lack of demand. Instead, it is experiencing more disciplined demand.

This is a selective-demand market, where success is determined less by overall activity and more by pricing accuracy and property positioning.

Minimal inventory and transaction volume mean trends are shaped by individual properties rather than market-wide forces.

Young remains one of the smallest and most variable markets in Rim Country, where trends are shaped by very limited transaction activity.

Micro-Market, Highly Variable Activity

🟣 $534,750

Average List Price

(+62.87% YoY)

🟢 4 vs 3

Active Listings

(+33%)

🟣 2 vs 0

Pending Sales (YTD)

🟢 0 vs 0

Closed Sales

🟣 Market Insight

This is a true micro-market.

Pricing and trends are driven by a handful of listings, not broad demand patterns.

In Young:

This creates large percentage swings:

This is a very low-volume, highly variable market, where:

Young is best understood as a micro-market, where trends should be interpreted cautiously and always in the context of extremely limited transaction volume.

Buyers are more selective, sellers face competition, and outcomes are increasingly tied to pricing and preparation.

This is the most important section. The data across all zip codes points to the same conclusion:

Not a speed-based market. Not a hype-based market. A professional market.

Increased listings and steady demand will reward agents who accurately interpret the market and guide client expectations.

In today’s market, strategy matters more than speed.

In a more balanced and nuanced environment, professional expertise is the defining advantage.

As we enter the spring market, the opportunity ahead is clear.

This is no longer a market driven by speed or momentum. It is a market defined by strategy, precision, and execution.

Buyers are active, but selective. Sellers are motivated, but facing increased competition. Success will depend on how well we interpret the data and guide our clients accordingly.

In this environment, the role of a REALTOR® becomes even more important.

Those who bring knowledge, preparation, and professionalism to every transaction will continue to lead.

And that is exactly what CAAR members do every day.

Interested in what CAAR does and how you can get involved? Contact us below to talk to our team.