Rim Country Short-Term Rental Market Update

By Central Arizona Association of REALTORS® President Dennis Riccio

Wildfire risk is increasingly being evaluated at the parcel level, including the home, roof, vents, decks, vegetation, and the first five feet around the structure.

Wildfire preparedness is no longer just a fire-season topic. It is becoming a real estate issue, an insurance issue, a lending issue, an affordability issue, and a property-value issue for homeowners throughout Rim Country.

For REALTORS®, this means wildfire preparedness can no longer be treated as background information. It may now affect whether a transaction can be insured, financed, and closed.

This issue is especially important in communities such as Payson, Pine, Strawberry, Star Valley, Christopher Creek, and other forest-adjacent areas where vegetation, topography, access, water supply, distance from fire services, and nearby forest conditions may all affect wildfire risk.

This past weekend, I had the opportunity to participate in the Northern Gila Fire Chiefs’ 2nd annual Wildfire Symposium as a representative of the local real estate community and as President of the Central Arizona Association of REALTORS®. The event brought together fire professionals, forest management experts, public safety officials, utility representatives, insurance professionals, and community stakeholders to discuss wildfire risk and the practical steps our communities can take to become more resilient.

One of the most important takeaways was this: wildfire risk must be addressed at more than one level. Forest health matters. Community planning matters. Fire response matters. Utilities and infrastructure matter. But the condition of the individual home and the first several feet around it may be one of the most important factors in whether that home survives.

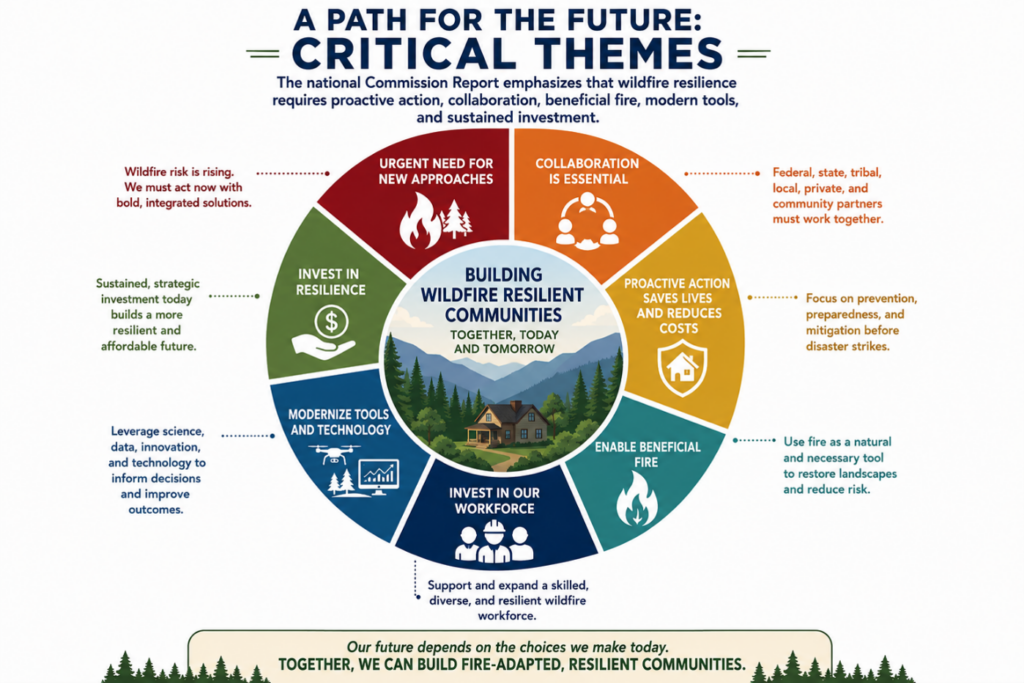

That message is consistent with the national Wildland Fire Mitigation and Management Commission’s report, which emphasized that wildfire is no longer simply a land management problem. It now directly affects public safety, public health, infrastructure, housing, insurance, recovery, local economies, and the built environment.

In other words, wildfire is not just a forest issue. It is a community issue.

Generations of fire suppression changed forest structure, increasing the need for both forest restoration and home-level mitigation.

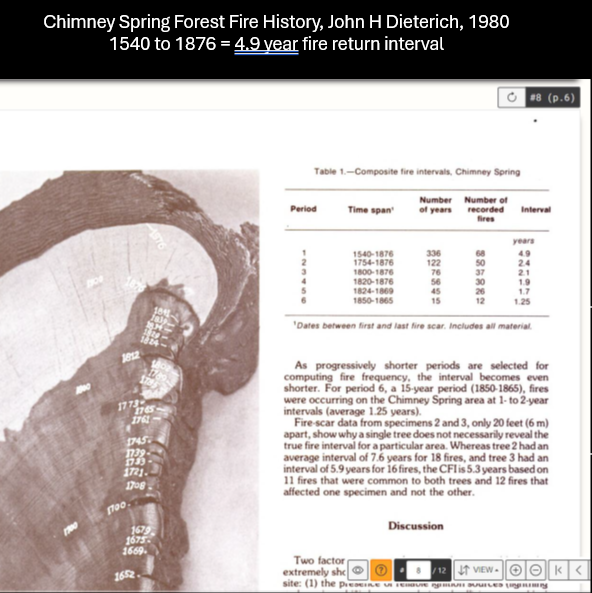

Neil Chapman, Wildland Fire Captain with the Flagstaff Fire Department, provided important context about how our forests reached their current condition. His presentation explained that fire suppression and exclusion in northern Arizona began around 1876. Historically, fire returned frequently to many northern Arizona ponderosa pine forests. The Chimney Spring fire history study referenced in his presentation found a fire return interval of approximately 4.9 years between 1540 and 1876.

That frequent fire helped maintain a more open, fire-adapted forest structure. With fire excluded for generations, many forests became denser and more vulnerable to severe fire. Mr. Chapman’s presentation identified several consequences of altered forest structure, including reduced water yield from watersheds, increased potential for insect outbreaks, reduced forage production and understory diversity, reduced habitat quality for many wildlife species, and increased potential for severe and large crown fires.

This is why landscape-scale wildfire risk reduction remains essential. Thinning, prescribed fire, and other forest restoration work help protect watersheds, economies, and communities. We are fortunate that local, state, and federal partners continue to perform fuel reduction, prescribed fire, and forest restoration work around Rim Country.

But the symposium also made clear that forest treatments alone are not enough.

Mr. Chapman’s presentation separated natural-environment risk from built-environment risk. The forest may be treated, but a home can still ignite if embers land in pine needles on the roof, combustible mulch next to the siding, firewood stacked against the home, an unscreened vent, a wood fence attached to the house, or debris under a deck.

That is where the Wildfire Prepared Home program becomes important.

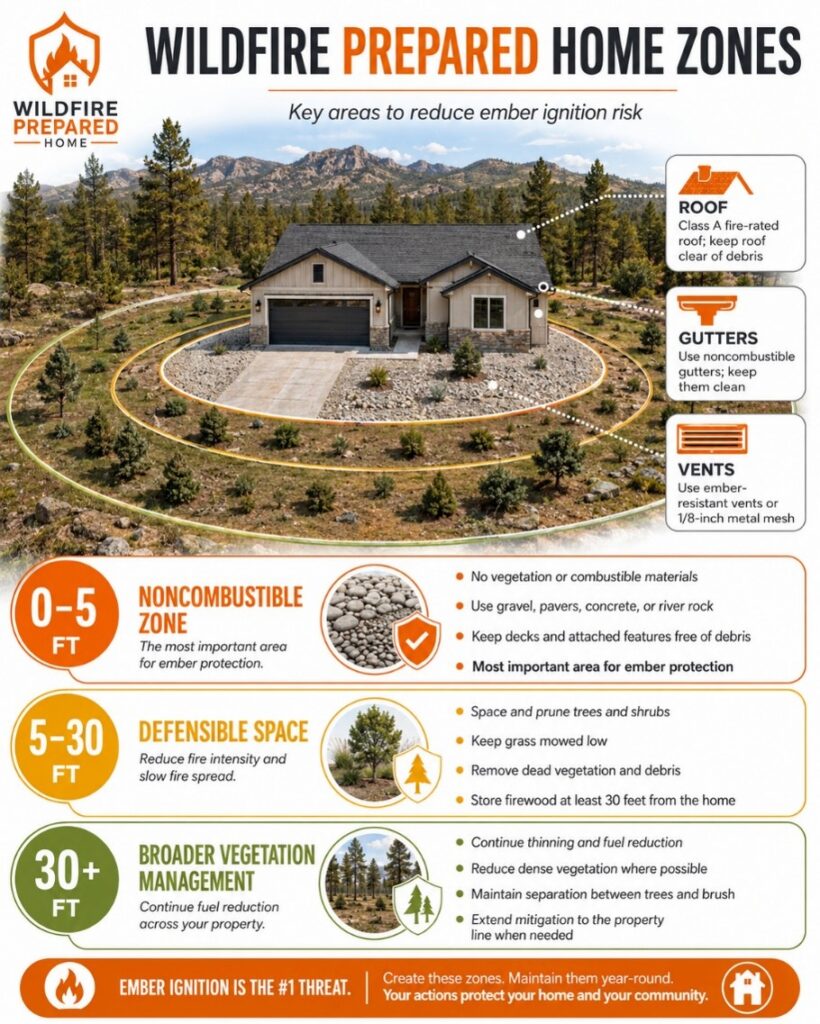

The Wildfire Prepared Home program provides a science-based framework for reducing the likelihood that a home will ignite during a wildfire event. The program focuses on the vulnerabilities that most often lead to home ignition, including defensible space, roofs, gutters, vents, decks, patios, fencing, siding, and combustible materials stored near the home.

The program includes two levels. The Base, or Essential, level focuses on protection from wind-blown embers, which are a leading cause of home ignition. The Plus, or Enhanced, level builds on the Base standard and adds additional protection from direct flame and radiant heat.

For most existing homes, the Base level may be the realistic starting point. Some of the most important steps include maintaining a 0-to-5-foot noncombustible zone around the home, keeping pine needles and leaves off roofs and out of gutters, using a Class A fire-rated roof covering, spacing vegetation properly from 5 to 30 feet, keeping firewood at least 30 feet from the home, and covering vents with appropriate ember-resistant materials or 1/8-inch corrosion-resistant metal mesh.

The Commission Report reinforces this same point. Decades of research have shown the importance of ignition-resistant construction, vegetation conditions around a structure, and the proximity of structures to one another. The report also notes that built-environment mitigation, such as replacing wood shake roofs, removing vegetation immediately adjacent to structures, and using ignition-resistant materials, can help prevent an initial loss and reduce the chance that fire spreads from structure to structure.

This distinction matters. Firewise communities play an important role in education, organization, and neighborhood action. The Wildfire Prepared Home program is different because it focuses on whether an individual home and the area immediately surrounding it meet specific mitigation standards. For insurance and real estate purposes, that parcel-level focus may become increasingly important.

The first five feet around a home may be one of the most important areas for reducing ember ignition risk

During the open round table discussion, we discussed how insurance uncertainty can affect real estate transactions. In the past, many buyers waited until later in the escrow process to finalize insurance. That approach may no longer be safe.

In some cases, buyers may discover that insurance is expensive, limited, or unavailable only after they are already under contract. This can affect inspections, loan approval, affordability, and the buyer’s willingness or ability to close.

Insurance should be addressed early in the transaction, not days before closing.

I also had a recent conversation with Eric Santana of a local State Farm branch in Payson. According to Mr. Santana, State Farm has begun requiring wildfire-related certification or compliance with fire-safe guidelines for many homes in the Payson area. His rough estimate was that approximately 10 to 15 percent of local homes may be difficult for State Farm to insure, approximately 20 percent may be insured without significant issue, and the remaining majority may need to meet wildfire safety guidelines before coverage is available. He also indicated that he expects this issue to grow and believes REALTORS® should be aware of it.

Those figures were shared as informal local observations and should not be understood as official State Farm underwriting guidelines, a companywide position, or a guarantee of coverage. However, the trend is important. Insurance companies are paying closer attention to wildfire risk, and REALTORS® should be prepared for that reality.

Insurance should be addressed early in the transaction, not days before closing.

The Commission Report also highlights why this issue has national importance. The report states that private insurers in the United States paid more than $50 billion in wildfire losses between 2017 and 2022. It also notes that wildfire response costs are only part of the overall financial burden. Local governments, businesses, homeowners, utilities, water systems, tourism, health care, and property values can all be affected.

That is why wildfire preparedness is now part of the real estate conversation.

A major theme of the Commission Report is the need to shift from a reactive wildfire system to a proactive one. Historically, much of the funding and attention has gone toward responding after fires start. The Commission recommends greater investment in planning, mitigation, community risk reduction, and resilience before disaster occurs.

That point should resonate with REALTORS®. We see the same principle in transactions every day. A roof issue is easier to address before escrow than during a loan delay. A septic issue is easier to address before closing than after a buyer objects. Insurance should be treated the same way.

The proactive approach is not only about public policy. It is also about individual homeowners, sellers, buyers, and agents taking practical steps before a problem affects a transaction.

The Commission Report also recognized that built-environment wildfire resilience has historically received less attention than natural-environment fuel reduction. That is changing. Going forward, successful wildfire policy will need to include both forest treatments and home-level mitigation.

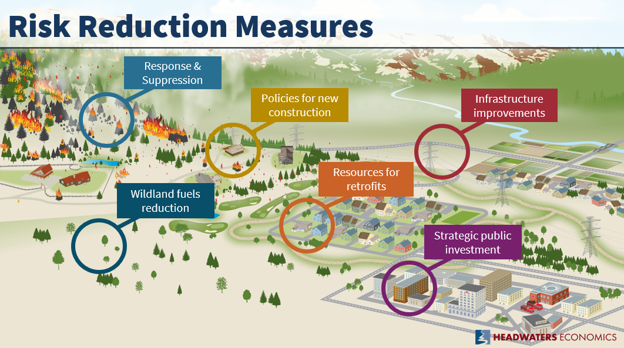

Mr. Chapman’s presentation made a similar point by identifying several categories of risk reduction: response and suppression, policies for new construction, infrastructure improvements, wildland fuels reduction, strategic public investment, and resources for retrofits. That is a useful framework for Rim Country. We need all of those pieces working together.

Wildfire risk reduction requires multiple tools working together, including response and suppression, new construction policies, infrastructure improvements, wildland fuels reduction, strategic public investment, and retrofit resources.

The national Commission Report emphasizes that wildfire resilience requires proactive action, collaboration, beneficial fire, modern tools, and sustained investment.

For REALTORS®, the practical takeaway is straightforward: wildfire preparedness should be addressed early, documented carefully, and referred to the appropriate professionals.

REALTORS® should encourage buyers to verify insurance availability and cost as early as possible, preferably during the inspection period. Listing agents should encourage sellers to address obvious wildfire hazards before going on the market. Agents should avoid giving insurance, fire-code, or mitigation opinions outside their expertise, but should be prepared to refer clients to qualified insurance professionals, fire officials, and mitigation resources.

Wildfire preparedness should now be treated as part of transaction risk management, much like roof condition, septic issues, flood risk, financing concerns, or homeowners association restrictions.

REALTORS® should also understand that this issue may affect affordability. If insurance premiums rise sharply, the buyer’s monthly payment may increase. In some cases, insurance cost may affect loan qualification. In other cases, insurance uncertainty may affect whether a buyer is willing to proceed.

For buyers, insurance should be addressed early in the transaction. Buyers should be encouraged to contact their insurance professional before the end of the inspection period. They should ask not only whether coverage is available, but whether wildfire coverage is included, whether any exclusions apply, whether mitigation is required, whether the premium could affect loan qualification, and whether the property may need to meet any wildfire safety standard before coverage is issued.

Buyers should also carefully review whether wildfire coverage is included or excluded. A policy that satisfies a lender’s basic requirement may not necessarily provide the level of protection the buyer assumes.

For sellers, wildfire preparedness may become part of preparing a home for market. Just as sellers often address roof issues, deferred maintenance, pest concerns, or curb appeal before listing, they may also need to consider visible wildfire hazards.

A clean roof, clear gutters, defensible space, properly screened vents, removal of combustible materials near the home, and relocation of firewood away from the structure may help reduce buyer concerns and avoid insurance surprises during escrow.

Sellers should also understand that visible wildfire hazards may affect marketability. Pine needles on the roof, combustible materials against the house, wood piles near the structure, unscreened vents, overgrown vegetation, combustible fencing attached to the home, and debris under decks may no longer be minor maintenance issues. They may affect whether a buyer can obtain affordable insurance.

This issue also affects new construction and community planning. Mr. Chapman’s presentation emphasized that new development, when planned appropriately, can decrease community-wide wildfire risk. The Commission Report also recognized that where development occurs, how homes are built, how close structures are to one another, and whether communities adopt science-based building standards can all influence wildfire outcomes.

That does not mean every community should adopt the same rule or that every home can meet the highest standard overnight. But it does mean wildfire risk should be part of discussions about subdivision design, access, water supply, defensible space, building materials, roofing, siding, fencing, decks, and evacuation planning.

The real estate community should be part of that conversation.

Simple steps now can improve safety and insurability.

The good news is that homeowners are not powerless. Many of the most important mitigation steps are practical and achievable. Some improvements can be expensive, but many meaningful steps are low-cost or no-cost, such as clearing roofs and gutters, removing pine needles, relocating firewood, improving the first 0-to-5 feet around the home, and reducing combustible materials near the structure.

For our broader community, the message is even more significant. Insurability is not only a private issue between a homeowner and an insurance company. If insurance becomes difficult or unaffordable, it can affect home sales, lending, affordability, property values, tax revenues, and community stability.

The symposium reinforced a simple but important point: Rim Country can remain a beautiful and desirable place to live, but we must learn to live responsibly with wildfire risk. Insurability is not only a private issue between a homeowner and an insurance company. If insurance becomes difficult or unaffordable, it can affect home sales, lending, affordability, property values, tax revenues, and community stability.

For REALTORS®, wildfire preparedness is now part of the real estate conversation. The more we understand it, the better we can serve our clients, protect transactions, and support the long-term resilience of our communities. Wildfire preparedness is no longer just about protecting homes from fire. It is about protecting transactions, affordability, insurability, property values, and the long-term stability of the communities we serve.

Interested in what CAAR does and how you can get involved? Contact us below to talk to our team.